All Categories

Featured

Table of Contents

For many individuals, the greatest issue with the limitless banking concept is that first hit to early liquidity triggered by the prices. Although this con of boundless financial can be lessened substantially with correct plan layout, the first years will certainly constantly be the worst years with any kind of Whole Life policy.

That said, there are particular infinite banking life insurance policy policies developed primarily for high very early cash value (HECV) of over 90% in the first year. The lasting performance will often significantly delay the best-performing Infinite Financial life insurance coverage policies. Having access to that added four figures in the very first couple of years may come with the price of 6-figures down the road.

You really get some significant lasting benefits that aid you recover these early expenses and afterwards some. We discover that this impeded early liquidity issue with infinite financial is much more mental than anything else when extensively checked out. In truth, if they definitely required every cent of the cash missing from their unlimited banking life insurance coverage plan in the initial couple of years.

Tag: infinite banking concept In this episode, I speak concerning funds with Mary Jo Irmen that instructs the Infinite Banking Concept. This subject might be debatable, but I wish to obtain diverse sights on the show and discover regarding different approaches for ranch economic administration. Some of you might agree and others will not, yet Mary Jo brings an actually... With the rise of TikTok as an information-sharing system, financial recommendations and techniques have located an unique means of spreading. One such strategy that has actually been making the rounds is the infinite banking concept, or IBC for brief, gathering endorsements from celebrities like rap artist Waka Flocka Flame. While the method is presently prominent, its origins trace back to the 1980s when financial expert Nelson Nash introduced it to the world.

Within these policies, the money worth grows based upon a price established by the insurer. When a considerable cash value gathers, insurance holders can get a cash money value loan. These loans differ from standard ones, with life insurance policy serving as security, meaning one could shed their coverage if loaning excessively without adequate cash worth to support the insurance prices.

And while the attraction of these plans appears, there are natural restrictions and threats, requiring diligent money value monitoring. The method's legitimacy isn't black and white. For high-net-worth individuals or company owners, specifically those making use of approaches like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance growth might be appealing.

Bank On Yourself Concept

The allure of infinite financial doesn't negate its challenges: Price: The fundamental demand, a permanent life insurance coverage plan, is more expensive than its term equivalents. Eligibility: Not every person gets approved for whole life insurance policy due to strenuous underwriting procedures that can omit those with certain health or way of life conditions. Complexity and risk: The elaborate nature of IBC, combined with its dangers, may prevent many, particularly when simpler and much less high-risk choices are available.

Allocating around 10% of your month-to-month earnings to the policy is just not feasible for lots of people. Making use of life insurance policy as an investment and liquidity resource calls for self-control and surveillance of plan money worth. Seek advice from a financial consultant to establish if boundless banking lines up with your concerns. Component of what you review below is merely a reiteration of what has actually currently been claimed over.

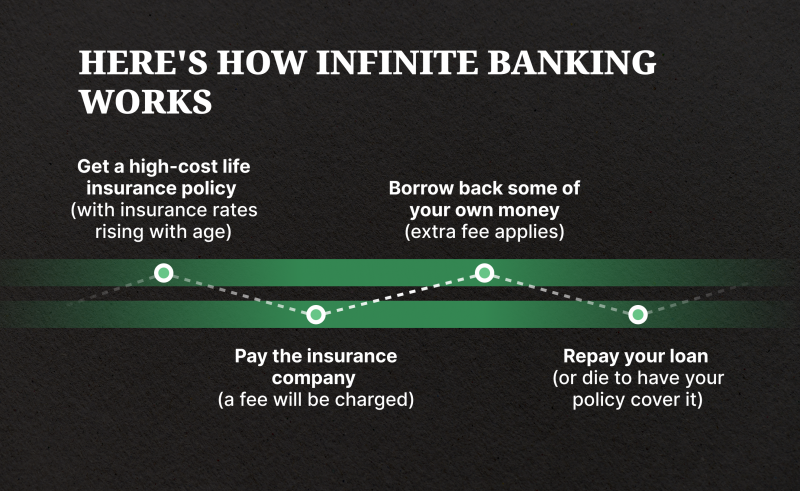

So prior to you get on your own right into a scenario you're not gotten ready for, understand the adhering to first: Although the concept is typically sold thus, you're not actually taking a loan from yourself. If that were the instance, you wouldn't need to settle it. Instead, you're borrowing from the insurer and need to settle it with rate of interest.

Some social media blog posts suggest using cash money worth from entire life insurance to pay down bank card financial obligation. The concept is that when you repay the funding with interest, the amount will be returned to your financial investments. Sadly, that's not just how it works. When you pay back the loan, a section of that rate of interest mosts likely to the insurer.

For the first several years, you'll be paying off the payment. This makes it exceptionally tough for your policy to accumulate worth during this time. Unless you can afford to pay a couple of to several hundred dollars for the next years or even more, IBC will not function for you.

Infinite Banking Think Tank

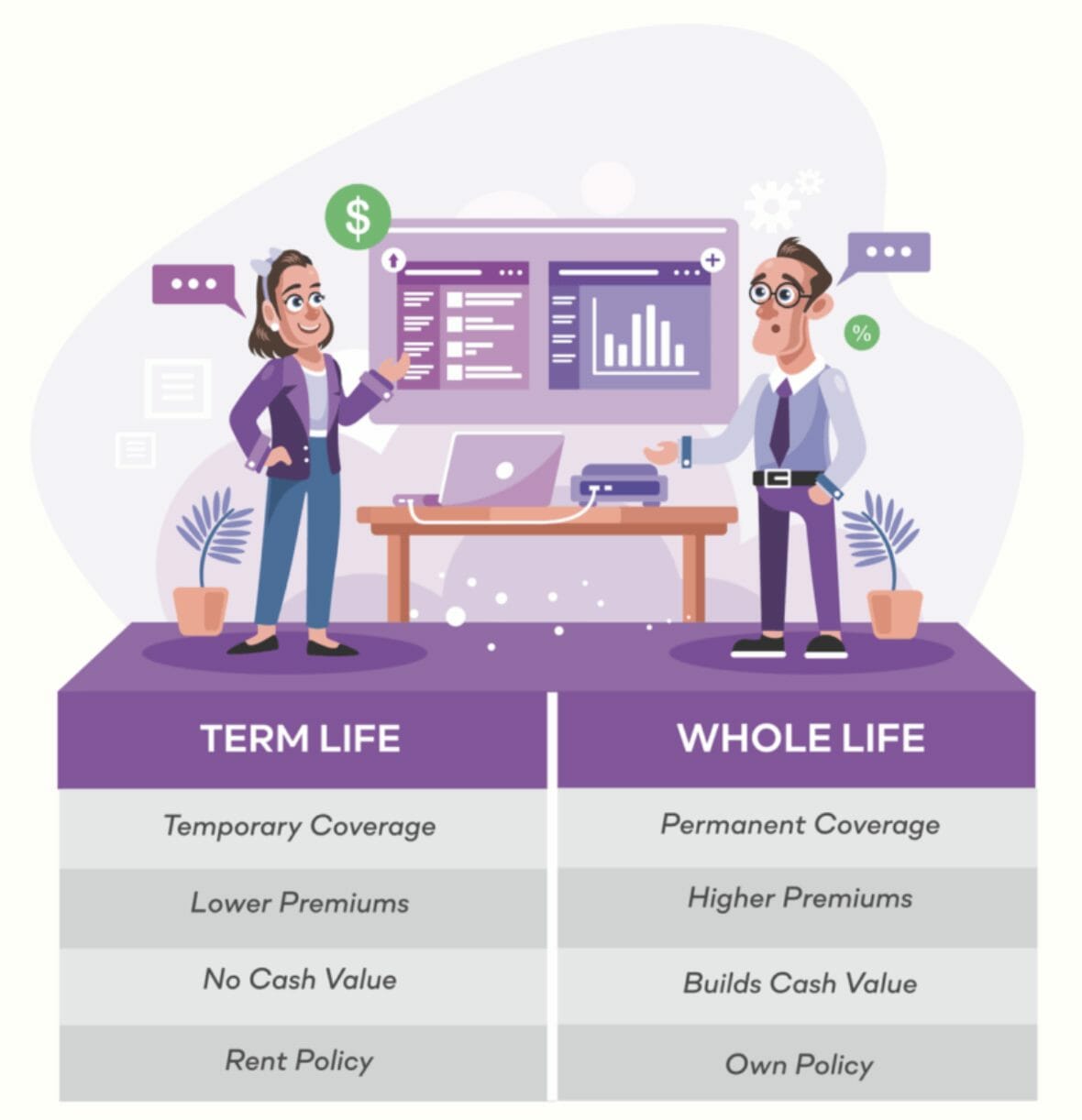

If you need life insurance, below are some useful tips to take into consideration: Take into consideration term life insurance coverage. Make sure to shop around for the finest rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Font Name "Montserrat". This Font style Software application is licensed under the SIL Open Up Font Certificate, Variation 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Typeface Name "Montserrat". This Font Software program is licensed under the SIL Open Up Typeface License, Variation 1.1.Skip to primary material

Infinite Banking Concept Explained

As a CPA specializing in realty investing, I've combed shoulders with the "Infinite Banking Concept" (IBC) a lot more times than I can count. I've also spoken with specialists on the topic. The major draw, besides the noticeable life insurance policy advantages, was constantly the idea of developing up cash money worth within an irreversible life insurance policy policy and loaning against it.

Certain, that makes good sense. Honestly, I always believed that cash would certainly be better invested straight on financial investments rather than channeling it via a life insurance coverage plan Until I uncovered how IBC can be incorporated with an Irrevocable Life Insurance Policy Trust (ILIT) to produce generational wealth. Let's begin with the basics.

Become Your Own Bank

When you obtain against your plan's cash money worth, there's no set settlement routine, providing you the flexibility to handle the financing on your terms. The cash value continues to expand based on the policy's warranties and returns. This configuration allows you to accessibility liquidity without disrupting the long-lasting growth of your policy, gave that the loan and rate of interest are managed carefully.

The procedure proceeds with future generations. As grandchildren are born and expand up, the ILIT can buy life insurance policy policies on their lives too. The depend on then collects several plans, each with expanding cash worths and survivor benefit. With these plans in place, the ILIT successfully comes to be a "Household Bank." Member of the family can take finances from the ILIT, using the money worth of the policies to fund investments, start companies, or cover significant expenses.

An important facet of managing this Family members Bank is using the HEMS standard, which stands for "Wellness, Education And Learning, Upkeep, or Support." This guideline is often consisted of in trust arrangements to guide the trustee on how they can disperse funds to recipients. By adhering to the HEMS requirement, the trust fund guarantees that circulations are produced necessary needs and long-lasting support, safeguarding the trust's assets while still providing for relative.

Increased Adaptability: Unlike stiff small business loan, you manage the settlement terms when obtaining from your very own policy. This enables you to structure repayments in a manner that straightens with your service capital. alliance bank visa infinite. Better Cash Circulation: By funding overhead via policy finances, you can potentially liberate cash that would otherwise be connected up in traditional car loan settlements or equipment leases

He has the same tools, yet has likewise constructed additional money value in his plan and received tax benefits. Plus, he now has $50,000 available in his policy to utilize for future opportunities or costs. Despite its potential advantages, some individuals stay doubtful of the Infinite Financial Concept. Let's resolve a couple of common concerns: "Isn't this simply expensive life insurance?" While it's real that the costs for a correctly structured whole life policy might be more than term insurance, it's vital to watch it as greater than just life insurance policy.

Infinite Concept

It has to do with creating an adaptable financing system that provides you control and offers several benefits. When utilized tactically, it can enhance various other investments and company strategies. If you're captivated by the potential of the Infinite Banking Idea for your organization, here are some actions to take into consideration: Educate Yourself: Dive much deeper right into the idea with trusted books, seminars, or examinations with well-informed specialists.

{kind=link}

Latest Posts

How To Train Yourself To Financial Freedom In 5 Steps

Infinite Banking Canada

My Wallet Be Your Own Bank